Wise Bookkeeper Blog

Why Your Jobs Look Profitable, but Your Bank Account Disagrees

Why Your Jobs Look Profitable, but Your Bank Account Disagrees

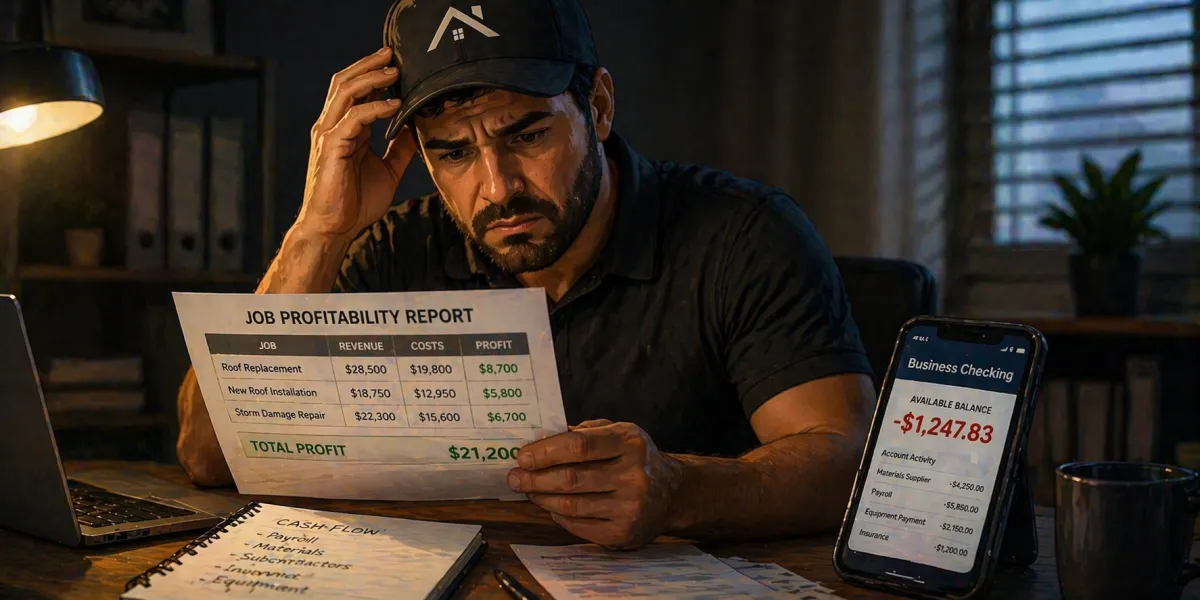

You finished the job.

The numbers look good.

On paper, you made money.

So why does your bank account tell a completely different story?

If you’ve ever looked at a “profitable” month and still felt cash-strapped, you’re not alone.

This is one of the most common and frustrating issues roofing company owners face.

Because profit and cash are not the same thing.

The Core Problem: Profit vs. Cash

Your financial reports (like your Profit & Loss statement) measure profit.

Your bank account reflects cash.

And the two don’t always move together.

Here’s the simplest way to think about it:

Profit = Revenue earned minus expenses incurred

Cash = Money actually moving in and out of your bank

👉 You can be profitable on paper and still run out of cash.

Why This Happens in Roofing Businesses

Roofing companies are especially prone to this disconnect because of how money flows through jobs.

Let’s break down the most common causes.

1. Timing Differences (The Biggest Culprit)

You might record revenue when a job is completed, but not get paid until weeks later.

At the same time:

Materials were already purchased

Labor was already paid

So your P&L shows profit…

But your cash is already gone.

👉 Timing, not profitability, is often the issue.

2. Accounts Receivable (Money You Haven’t Collected Yet)

If your reporting is on an accrual basis, that “profit” on your books may include invoices that haven’t been paid.

If customers are slow to pay, your financials can look strong while your cash flow suffers.

Warning signs:

Growing list of unpaid invoices

Longer payment cycles

Cash feeling tight despite strong sales

👉 Revenue doesn’t count as cash until it’s collected.

3. Upfront Costs on Jobs

Roofing jobs often require significant upfront spending:

Materials

Dump fees

Labor

If your payment structure doesn’t match your cost structure, you’re funding jobs out of pocket.

👉 If cash goes out before it comes in, you’ll feel the squeeze.

4. Debt and Equipment Payments

Your P&L may not fully reflect certain cash outflows, like:

Loan payments (principal portion)

Equipment purchases

Truck payments

Owner cash withdrawn (disbursements)

These don’t always show up as expenses in the way you expect, but they absolutely impact your bank balance.

👉 Not all cash outflows show up clearly on your profit report.

5. Taxes You Haven’t Paid Yet

Your P&L might show a healthy profit, but that also means you owe taxes.

If you’re not setting money aside, your “profit” isn’t fully yours.

👉 Unplanned taxes can quickly drain your cash.

6. Overhead Creep

You might be making money on jobs, but slowly losing it elsewhere.

Admin costs increase

Software subscriptions stack up

Fuel and operational costs rise

Individually, they don’t seem like much, but together, they eat into your cash.

👉 Profit leaks often happen outside the job itself.

How to Spot the Disconnect Early

The goal isn’t just to understand the problem, it’s to catch it before it hurts you.

Here’s what to watch:

1. Profit is up, but cash is flat (or down)

This is your biggest red flag.

2. Receivables are growing

More unpaid invoices = more pressure on cash.

3. You’re relying on credit to cover expenses

If you’re borrowing to stay afloat during “profitable” periods, something’s off.

4. You’re surprised by your bank balance

Surprises mean you don’t have visibility.

👉 If your numbers don’t match your reality, dig deeper.

How to Fix It

You don’t need a complicated system; you need better alignment between profit and cash.

1. Improve Your Payment Structure

Collect deposits upfront

Use progress billing for larger jobs

Don’t wait until the end to get paid

👉 Match your inflows to your outflows.

2. Stay on Top of Collections

Review receivables weekly

Follow up consistently

Set clear payment expectations

👉 Faster collections = stronger cash flow.

3. Build a Cash Flow Forecast

Know what’s coming before it hits.

Map out expected inflows and outflows

Identify tight weeks in advance

Adjust early

👉 Visibility eliminates surprises.

4. Track Job Profitability and Cash Impact Separately

A job can be profitable, but still hurt your cash if timing is off.

Look at both:

Job margin

Cash timing

👉 Profit tells you if it’s worth doing. Cash tells you if you can sustain it.

5. Set Aside Money for Taxes

Don’t treat all profit as spendable.

Even a simple system, like moving a percentage to a separate account, can prevent future stress.

The Bottom Line

If your jobs look profitable but your bank account disagrees, the issue isn’t necessarily your business.

It’s your visibility into how money actually moves.

Because:

Profit is a snapshot

Cash flow is a timeline

And in roofing, timing is everything.

Final Thought

You don’t build a strong business by just being profitable.

You build it by keeping the cash that profit is supposed to create.

When you understand the difference and manage both, you move from guessing to being in control.

Want Help Connecting the Dots?

At Wise Bookkeeper, we help roofing companies bridge the gap between profit and real cash flow.

So your numbers don’t just look good on paper, they work in real life.

Let’s bring clarity back to your business.

© 2024 Very Good Business Services

Contact

kendra@wisebookkeeper.com

888-705-9609